In this article, three approaches to smooth data will be demonstrated:

- standard polynomial regression

- cubic B-spline regression

- smoothing splines

The data will a set of loss development factors (LDFs) associated with an unidentified line of business. Instead of smoothing LDFs patterns directly, we first compute the cumulative loss development factors (CLDFs), then take the reciprocal to obtain Percent of Ultimate factors. Doing so will generally (not always) result in a monotonically increasing factor as a function of time. The code that follows prepares our data:

library("data.table")

library("ggplot2")

options(scipen=9999)

ldfs = c(

2.85637, 1.58402, 1.37531, 1.3001, 1.21469, 1.28128, 1.15415, 1.09783, 1.09302,

1.06395, 1.04992, 1.04659, 1.05164, 1.03117, 1.0236, 1.06338, 1.03234, 1.0172,

1.01795, 1.01813, 1.01413, 1.00863, 1.01346, 1.00372, 1.00423, 1.00683, 1.04633,

1.01796, 1.02279, 1.00629, 1.00205, 1.00316, 1.007, 1.02828, 1.00117, 1.00303,

1.00055, 1.02272, 1.00678, 1.00152, 1.00013, 1.01347, 1, 1.00071, 1.00136

)

# Compute cumulative development factors.

cldfs = rev(cumprod(rev(ldfs)))

# Compute percent-of-ultimate factors.

pous = 1 / cldfs

DF = data.table(

xinit=1:length(pous), ldf0=ldfs, cldf0=cldfs, y=pous,

stringsAsFactors=FALSE

)

# Rescale `dev` to fall between 0-1.

DF[,x:=seq(0, 1, length.out=nrow(DF))]

setcolorder(

DF, c("xinit", "x", "y", "ldf0", "cldf0")

)Fields in DF are defined as follows:

xinit: Original development period. 1 <=xinit<= 45.x:xinitrescaled to [0,1].y: Percent-of-ultimate factors.ldf0: Original unsmoothed loss development factors.cldf0: Original unsmoothed cumulative loss development factors.

Inspecting our data yields:

xinit x y ldf0 cldf0

1: 1 0.00000000 0.03022475 2.85637 33.085464

2: 2 0.02272727 0.08633308 1.58402 11.583045

3: 3 0.04545455 0.13675333 1.37531 7.312436

4: 4 0.06818182 0.18807822 1.30010 5.316937

5: 5 0.09090909 0.24452049 1.21469 4.089637

6: 6 0.11363636 0.29701659 1.28128 3.366815

7: 7 0.13636364 0.38056142 1.15415 2.627697

8: 8 0.15909091 0.43922497 1.09783 2.276738

9: 9 0.18181818 0.48219434 1.09302 2.073853

10: 10 0.20454545 0.52704806 1.06395 1.897360

11: 11 0.22727273 0.56075279 1.04992 1.783317

12: 12 0.25000000 0.58874556 1.04659 1.698527

13: 13 0.27272727 0.61617522 1.05164 1.622915

14: 14 0.29545455 0.64799451 1.03117 1.543223

15: 15 0.31818182 0.66819250 1.02360 1.496575

16: 16 0.34090909 0.68396184 1.06338 1.462070

17: 17 0.36363636 0.72731134 1.03234 1.374927

18: 18 0.38636364 0.75083259 1.01720 1.331855

19: 19 0.40909091 0.76374691 1.01795 1.309334

20: 20 0.43181818 0.77745617 1.01813 1.286246

21: 21 0.45454545 0.79155145 1.01413 1.263342

22: 22 0.47727273 0.80273607 1.00863 1.245739

23: 23 0.50000000 0.80966368 1.01346 1.235081

24: 24 0.52272727 0.82056176 1.00372 1.218677

25: 25 0.54545455 0.82361425 1.00423 1.214161

26: 26 0.56818182 0.82709813 1.00683 1.209046

27: 27 0.59090909 0.83274721 1.04633 1.200845

28: 28 0.61363636 0.87132839 1.01796 1.147673

29: 29 0.63636364 0.88697745 1.02279 1.127424

30: 30 0.65909091 0.90719167 1.00629 1.102303

31: 31 0.68181818 0.91289790 1.00205 1.095413

32: 32 0.70454545 0.91476934 1.00316 1.093172

33: 33 0.72727273 0.91766001 1.00700 1.089728

34: 34 0.75000000 0.92408363 1.02828 1.082153

35: 35 0.77272727 0.95021672 1.00117 1.052392

36: 36 0.79545455 0.95132847 1.00303 1.051162

37: 37 0.81818182 0.95421100 1.00055 1.047986

38: 38 0.84090909 0.95473581 1.02272 1.047410

39: 39 0.86363636 0.97642741 1.00678 1.024142

40: 40 0.88636364 0.98304759 1.00152 1.017245

41: 41 0.90909091 0.98454182 1.00013 1.015701

42: 42 0.93181818 0.98466981 1.01347 1.015569

43: 43 0.95454545 0.99793331 1.00000 1.002071

44: 44 0.97727273 0.99793331 1.00071 1.002071

45: 45 1.00000000 0.99864185 1.00136 1.001360

xinit x y ldf0 cldf0Smoothing via Polynomial Regression

Polynomial regression is similar to standard linear regression, except the design matrix contains x raised to the desired power in each column. For example, assuming we have independent value x given by:

x = c(2, 4, 7, 5, 2)Instead of regressing a response y on x alone, polynomial regression fits y using the matrix X:

1 2 3

[1,] 2 4 8

[2,] 4 16 64

[3,] 7 49 343

[4,] 5 25 125

[5,] 2 4 8Notice each column represents x raised to the power in the column header. The first column is \(x^{1}\), the second \(x^{2}\) and the third \(x^{3}\). Creating the design matrix in R can be accomplished using the poly function. Next we create the design matrix X and fit a polynomial regression model of degree 3 to our data:

X = poly(DF$x, degree=3, raw=TRUE)

y = DF$y

# Combine design matrix with target response y (pous).

DF1 = setDT(cbind.data.frame(X, y))

# Call lm function. On RHS of formula, `.` specifies all columns in DF1 are to be used.

mdl = lm(y ~ ., data=DF1)

# Bind reference to fitted values as yhat1.

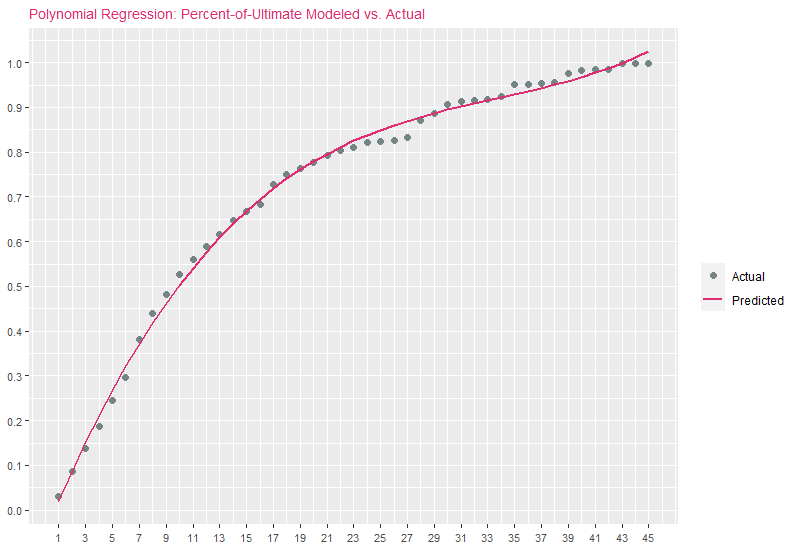

DF[,yhat1:=unname(predict(mdl))]A visualization overlaying polynomial regression estimates with original percent-of-ultimate factors is presented below (this code will be reused for all exhibits that follow, with inputs updated as necessary):

exhibitTitle = paste0("Polynomial Regression: Percent-of-Ultimate Modeled vs. Actual")

ggplot(DF) +

geom_point(aes(x=xinit, y=y, color="Actual"), size=2) +

geom_line(aes(x=xinit, y=yhat1, color="Predicted"), size=1.0) +

guides(color=guide_legend(override.aes=list(shape=c(16, NA), linetype=c(0, 1)))) +

scale_color_manual("", values=c("Actual"="#758585", "Predicted"="#E02C70")) +

scale_x_continuous(breaks=seq(min(DF$xinit), max(DF$xinit), 2)) +

scale_y_continuous(breaks=seq(0, 1, .1)) + ggtitle(exhibitTitle) +

theme(

plot.title=element_text(size=10, color="#E02C70"),

axis.title.x=element_blank(), axis.title.y=element_blank(),

axis.text.x=element_text(angle=0, vjust=0.5, size=8),

axis.text.y=element_text(size=8)

)

There is a generally good fit to actuals, but notice that for later development periods, estimates are increasing upward rather than leveling off asymptotically toward 1.0. This is one of the drawbacks of polynomial regression: The bases are non-local, meaning that the fitted value of \(y\) at a given value \(x=x_{0}\) depends strongly on data values for \(x\) far from \(x_{0}\). In modern statistical modeling applications, polynomial basis-functions are used along with new basis functions such as splines, introduced next.

Smoothing via B-Spline Regression

B-spline regression remedies the shortcomings of polynomial regression, namely the issue of non-locality. I’m going to demonstrate the usage of B-splines within the context of R rather than delve into the mathematical details. For an in-depth overview of B-splines, refer to Elements of Statistical Learning, specifically chapter 5.

To perform B-spline regression in R, the bs function is used to generate the B-spline basis matrix for a polynomial spline. The number of spline knots to use is specified, along with the degree of polynomial to use (defaults to 3). We then generate the knot locations using the range of our independent value (x) and the number of knots using the seq function. Techniques can be used to minimize a cost function, such as LOOCV to minimize average MSE in order to determine the optimal number of knots, but we omit this step and instead arbitrarily choose 5 knots for the purposes of demonstration. As a rule-of-thumb, more knots leads to higher variance and lower bias.

library("splines")

y = DF$y

nbrSplineKnots = 5

# Knot locations using data min/max and nbrSplineKnots.

knotsSeq = seq(min(DF$x), max(DF$x), length.out=nbrSplineKnots)

# Create basis matrix using splines::bs. degree=3 represents cubic spline.

Bbasis = bs(DF$x, knots=knotsSeq, degree=3)

# Drop columns containing only a single value.

Bbasis = as.matrix(Filter(function(v) uniqueN(v)>1, as.data.table(Bbasis)))

# Combine design matrix with target y (pous).

DF2 = setDT(cbind.data.frame(Bbasis, y))

# Fit B-spline regression model.

mdl2 = lm(y ~ ., data=DF2)

# Bind reference to fitted values as yhat2.

DF[,yhat2:=unname(predict(mdl2))]Running the same ggplot2 code from before, replacing yhat1 with yhat2, we obtain:

Polynomial regression and B-spline estimates are similar, but B-spline estimates exhibit better behavior in the later periods, with estimates far less influenced by erratic observations, while also approaching 1.0 on the right. The B-spline fit exhibits a good trade-off between bias and variance.

Smoothing via smooth.spline

\(\{x_{i},Y_{i}:i=1,\dots ,n\}\), which we model by \(Y_{i} = f(x_{i}) + \epsilon_{i}\), where \(\epsilon_{i}\) are zero mean random errors. The cubic smoothing spline estimate \(\hat{f}\) of the function \(f\) is defined to be the minimizer of:

\[ \sum _{i=1}^{n}[Y_{i}-{\hat {f}}(x_{i})]^{2}+\lambda \int {\hat {f}}''(x)^{2}dx, \]

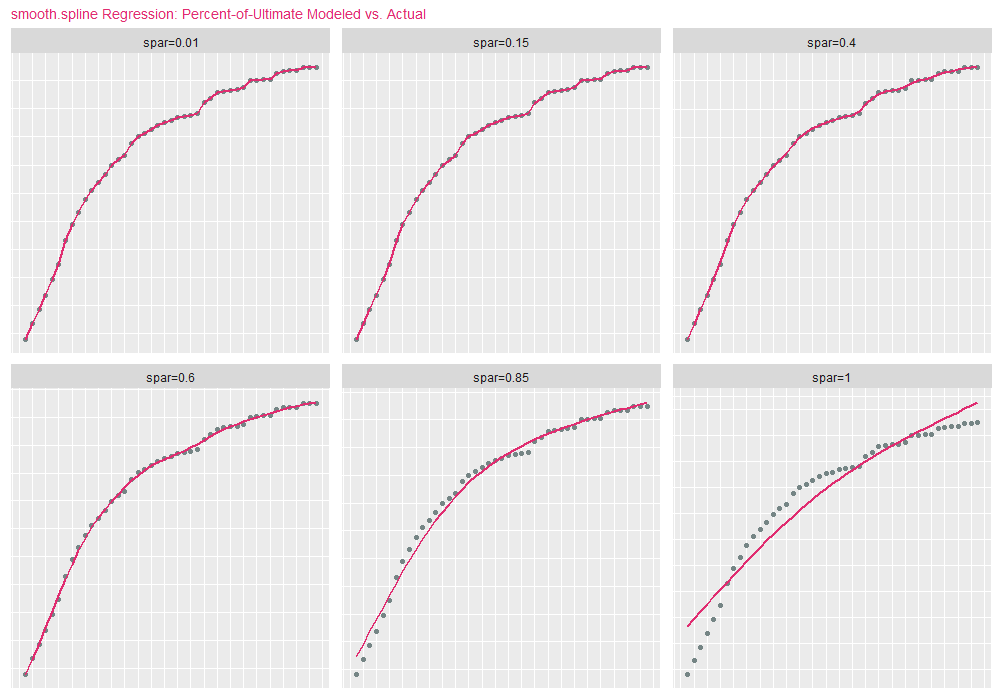

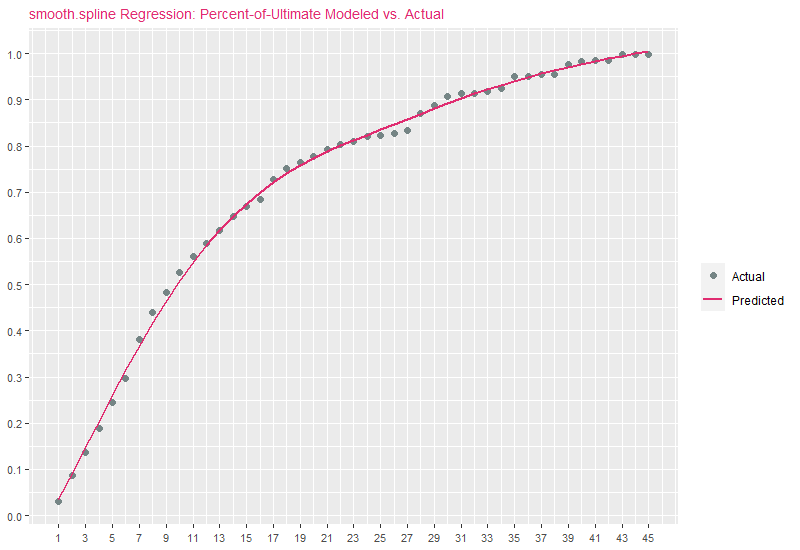

where \(\lambda \geq 0\) is a smoothing parameter wehich controls the bias variance trade-off. With respect to the smooth.spline function, \(\lambda\) is identified as spar, where 0 <= spar <=1. As spar approaches 1, the fit resembles linear regression (low variance / high bias). As spar approaches 0, the fit resembles interpolation (high variance / low bias). For the purposes of demonstration, we set spar=.70 and df (degrees of freedom) to the number of records in the data:

smoothParam = .70

yhat3 = smooth.spline(DF$x, DF$y, df=nrow(DF), spar=smoothParam)$y

DF[,yhat3:=yhat3]yhat3 vs. percent-of-ultimates:

It comes as no surprise that smooth.spline predictions are similar to B-spline estimates. To demonstrate how changing spar modifies the nature of the curve, we present the next code block, which fits the original percent-of-ultimate data using smooth.spline for 6 values of spar:

library("foreach")

targetSpar = c(.01, .15, .40 , .60, .85, 1.0)

DF3 = foreach(

i=1:length(targetSpar), .inorder=TRUE, .errorhandling="stop",

.final=function(ll) rbindlist(ll, fill=TRUE)

) %do% {

currSpar = targetSpar[[i]]

currDF = DF[,.(xinit, x, y)]

sparID = paste0("spar=", round(currSpar, 2))

mdl = smooth.spline(currDF[,x], currDF[,y], df=nrow(currDF), spar=currSpar)

currDF[,`:=`(yhat=mdl$y, id=sparID, spar=currSpar)]

}

ggplot(DF3) +

geom_point(aes(x=xinit, y=y, color="Actual"), size=1.5) +

geom_line(aes(x=xinit, y=yhat, color="Predicted"), size=.75) +

scale_color_manual("", values=c("Actual"="#758585", "Predicted"="#E02C70")) +

scale_x_continuous(breaks=seq(min(DF3$xinit), max(DF3$xinit), 2)) +

scale_y_continuous(breaks=seq(0, 1, .1)) +

facet_wrap(facets=vars(id), nrow=2, scales="free", shrink=FALSE) +

ggtitle("smooth.spline Regression: Percent-of-Ultimate Modeled vs. Actual") +

theme(

plot.title=element_text(size=10, color="#E02C70"),

axis.title.x=element_blank(), axis.title.y=element_blank(),

axis.text.x=element_blank(), axis.text.y=element_blank(),

legend.position="none", panel.grid.major=element_blank(),

axis.ticks=element_blank()

)spar=1 is the lower-right facet (lowest variance/highest bias), and spar=.01 the upper-left facet (highest variance/lowest bias):